Turn Back Time

As an investor, I’ve often wished I could jump on an opportunity I missed. For many investors, names like Apple and Amazon come to mind. If I could turn back the clock to 2000, I would buy both and retire rich.

If you listened to James Altucher years ago, you may have been fortunate enough to buy Bitcoin for around $1,000 and enjoyed a 100x return in just seven years.

More recently, you may be lamenting missing Microstrategy (MSTR). Michael Saylor has created a Bitcoin-equity behemoth. Check out the stock’s performance since 2020.

Although the stock struggled in 2022, its total return over the past five years is 2,485.73%, a massive move few saw coming.

Wouldn’t it be great to turn back the clock and buy Microstrategy before the market understood its unique business model?

What if I told you that you have a similar opportunity today? Maybe even better.

Introducing DeFi Technologies

DeFi Technologies (OTCQB: DEFTF) is a financial technology company leading the convergence of traditional capital markets with the world of decentralized finance (DeFi). Focusing on industry-leading Web3 technologies, DeFi Technologies aims to provide widespread investor access to the future of finance.

In short, the company has created simple and easy access to dozens of cryptocurrencies. Additionally, it provides many operations for the decentralized financial world we can find in traditional finance. The company operates diverse business segments, including DeFi infrastructure, crypto research, market making, asset management, venture investments, and arbitrage trading desk.

You’d be right if you think this sounds like a decentralized version of Blackrock or State Street.

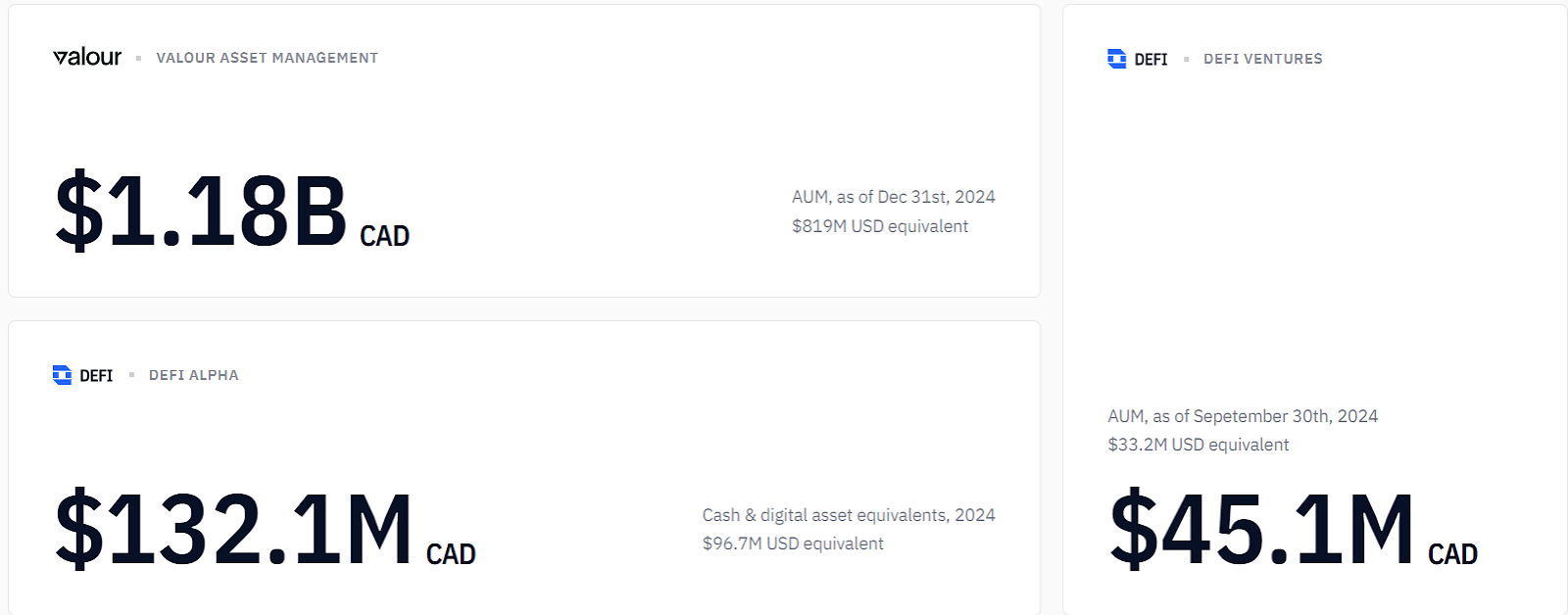

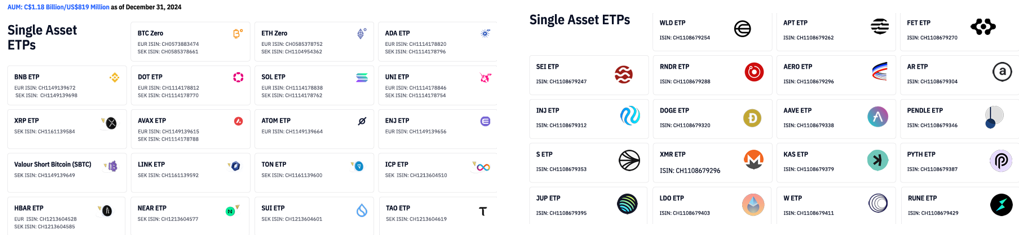

DeFi’s asset management segment, Valour, is the company’s crown jewel. Valour offers a portfolio of over 60 exchange-traded products (ETPs), Europe’s version of an ETF. Currently, the company focuses on the top 100 coins.

The company generates revenue from management fees and staking rewards received from holding and staking the underlying crypto assets. If the term staking is unfamiliar to you, think of it like the interest a bank would pay you on a certificate of deposit or a savings account.

The biggest benefit for shareholders is that DeFi allows investors to invest in roughly five dozen cryptocurrencies without speculating on a specific one.

Speculation on a single coin, Bitcoin, has propelled Microstrategy’s valuation to stratospheric heights. While DeFi Technologies doesn’t have the Bitcoin (BTC) on its balance sheet to replicate Microstrategy, it does have access to the Solana (SOL) it needs to become the Solana version of Microstrategy.

Management has already announced it will be spinning out SolFi Technologies to shareholders. Owning DEFTF now will get you shares of SoFi Technologies before they are trading standalone on the public markets.

Exploring SolFi Technologies and the Solana Ecosystem

DeFi Technologies has launched SolFi Technologies, a spinout that provides investors access to the fast-growing Solana blockchain ecosystem. SolFi combines innovative treasury strategies, staking operations, and ecosystem investments to generate high-yield returns and capitalize on Solana’s rapid adoption in the decentralized finance (DeFi) space.

Unlocking Solana’s Potential

Solana, known for its high transaction speed and scalability, has become a leading blockchain platform in 2024. The network processes over 65,000 transactions per second and recorded 42.7 million daily transactions in October—far surpassing Ethereum. Major corporations like Google, Stripe, Shopify, and PayPay have integrated Solana, validating its technological edge.

Memecoin mania has propelled Solana’s trading volume to record heights. In the first 72 hours of hectic trading, after Trump endorsed the official Trump coin, the Solana decentralized exchange (DEX) trading volume hit $28 billion on January 18th and $27 billion on January 19th. Both were all-time highs.

Solana’s DEX also reached nearly $17 billion on January 17th. The surge in volume has generated $35 million in fees this month. For comparison, the Nasdaq averages around $300 billion per day. Whether you believe in the validity of cryptocurrency and meme coins, the amount of money transacted daily is very real.

SolFi Technologies is perfectly positioned to benefit from this type of trading. The company accelerates growth by acquiring and staking Solana (SOL) tokens through proprietary trading algorithms and a Maximum Extractable Value (MEV) engine. This approach, tested with over $365 million in staked assets, delivers higher yields than third-party providers, generating consistent cash flows. These earnings are reinvested or distributed as dividends, offering investors an opportunity for compounding returns.

A Strategic Investment Vehicle

Positioned as the “MicroStrategy for Solana,” SolFi combines capital appreciation with operational cash flow, enabling investors to outperform traditional token holdings. Beyond staking, SolFi is diversifying through acquisitions of operating companies and investments in innovative projects within the Solana ecosystem, enhancing its treasury strategy. I’ll touch on this a bit more in the S.M.A.R.T. section of the report.

Why Invest in Solana and DeFi?

The broader DeFi market and Solana present a compelling growth story. With Solana’s token price surging tenfold in 2024 and 24-hour trading volumes exceeding $4 billion, it has become a hub for decentralized applications. Key platforms like Serum and Raydium highlight its strength.

The coin’s fully diluted value (FDV) is approaching $250 billion. When measured by market cap, it ranks among the top five cryptocurrencies. It consistently ranks in the top 10 in terms of trading volume. And with the explosion of meme coin trading, I anticipate Solana will maintain a top 5 trading volume rank in 2025, exclusive of stablecoins.

Check out Solana’s performance over the past four and a half years. In July 2020, you could have bought SOL for around $1. Today, it trades for $240. That’s a ten-times better return than Microstrategy over a similar time frame!

SolFi should outperform traditional token holdings courtesy of its proprietary below-market coin acquisition strategy and underlying cash-flowing operational company. As shareholders and partners, DEFTF holders can gain exposure to SolFi and Solana’s unparalleled ecosystem growth before the spinout and own a piece of the MicroStrategy for Solana before the broader market understands the stock’s true potential.

Solid Fundamentals

Assessing the fundamentals of a smaller company trading on the over-the-counter exchange presents a unique challenge. Traditional metrics can be applied, but the market will often discount them because of the exchange where the stock trades. For us, identifying those discounted companies, especially ones poised to uplist to a senior exchange, offers an asymmetric opportunity.

With a market cap approaching one billion, average daily trading volume of 1.4 million shares, and solid fundamentals, this name won’t remain on the OTC much longer. It appears destined for a Nasdaq listing. In fact, it already filed its Form 40-F back in September.

DeFi allows investors to benefit from roughly five dozen different cryptocurrencies without speculating on even one. The company showcases spectacular growth, strong net cash flow, and a blossoming balance sheet filled with cash and digital investments. All of this without the high risk that makes this sector famous.

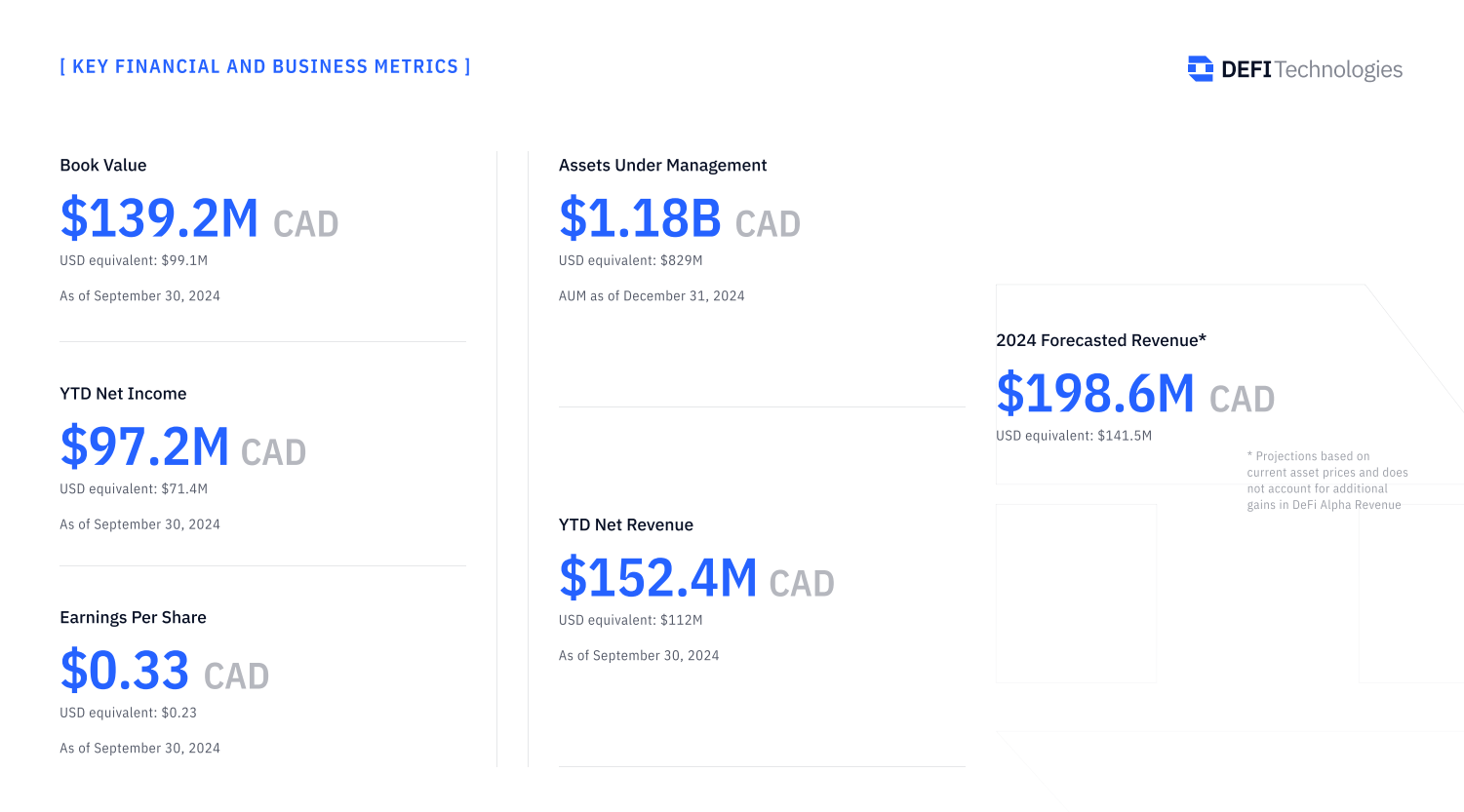

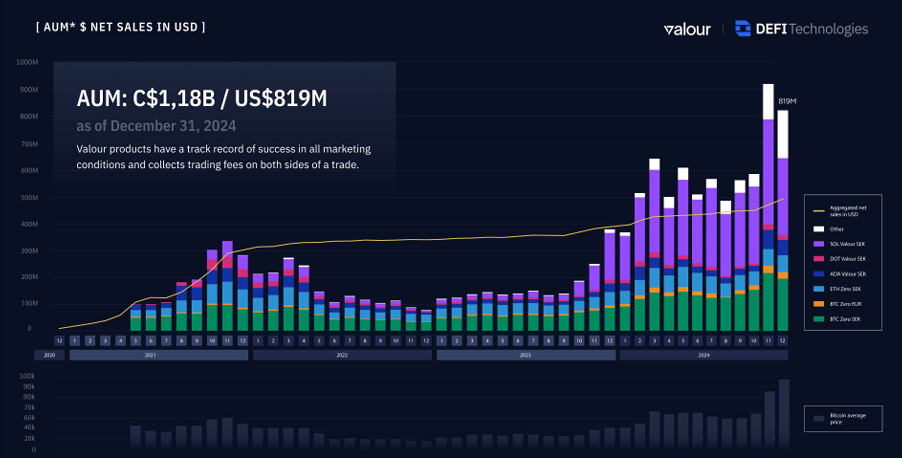

Assets under management (AUM) in the ETPs have exploded over the past two years. At the end of 2022, AUM stood at $106 million, rising to over $920 million less than two years later. Over the past two years, there hasn’t been a single month when AUM has not increased from the prior month. Given that DeFi launched 20 new ETPs in December, there’s a high probability AUM net inflows will continue to climb.

Management indicated they generate revenue of 8-10% on AUM. If AUM did not grow another penny, the company would be on pace for $80 million to $100 million in 2025. This is unlikely, given that the company has increased AUM monthly for two years, even during the crypto bear market.

When we factor in the $97.5 million in revenue DeFi’s arbitrage trading desk earned during the first 11 months of 2024, it’s reasonable to estimate that total revenues for 2025 could easily eclipse $200 million just from these two business segments. Note that these are low-risk arbitrage trades, not speculated day trades. The company takes advantage of marketplace inefficiencies. The trading desk has zero losses to date.

Management’s revenue projections of $141.5 million and net income of $71.4 million seem reasonable. These projections translate to earnings per share above $0.30 for the year.

These numbers put DEFTF at a trailing P/E below 9 and a price-to-sales ratio of 7. Neither RonbinHood (HOOD) nor Coinbase (COIN) can touch those numbers.

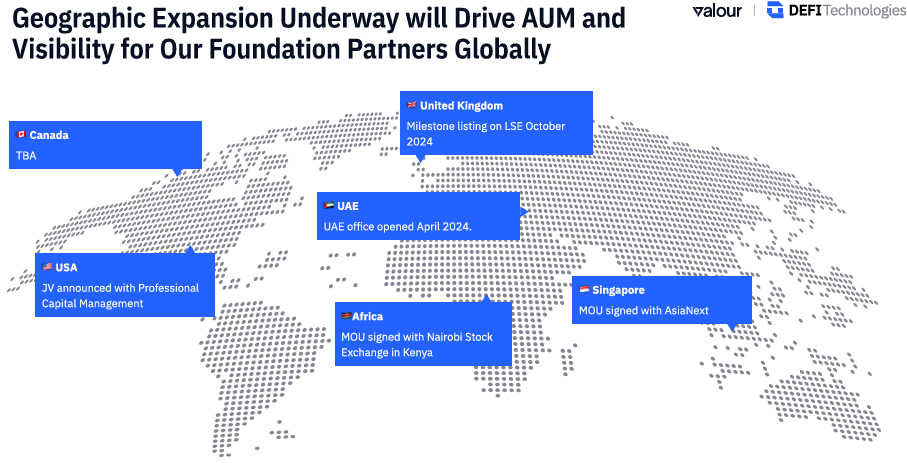

DeFi Technologies plans to launch another 40 ETPs in Europe next year and expand its business into Singapore, Africa, and the UAE. The company’s AUM could easily double next year.

DeFi has $6 million of debt on its balance sheet; however, that number doesn’t concern me given the cash and cash equivalent $15.2 million position it holds. Furthermore, as of December 31, 2024, DeFi held $40.7 million in digital assets. Those holdings are Bitcoin, Ethereum, Solana, Uniswap, Polkadot, Avalanche, Corechain, and more. I view virtually all their digital assets as readily liquid, so it is fair to say DeFi has net liquid assets (assets minus debt) of roughly $50 million.

Given its strong balance sheet, profitability, and positive cash flow, the dilution risk is minimal at the current price. The company could accelerate growth through acquisition; however, it possesses a strong enough balance sheet to do so with cash or in an accretive manner.

When I examine all these factors, DeFi Technologies enters 2025 with accelerating business momentum and a stock price that hasn’t kept pace. It is a unique blend of strong growth and deep value.

That has created an asymmetric opportunity for small-cap traders in a company that breaks the mold for its industry.

Management

Olivier Roussy Newton – Chairman & Chief Executive Officer

Olivier Francois Roussy Newton is the founder of DeFi Technologies, Inc. (founded in 1986), where he currently holds the title of Chairman & Chief Executive Officer. He was also the founder of HIVE Digital Technologies Ltd. in 1987, where he held the title of Independent Director. In addition, he founded Valour Structured Products, Inc. in 2018 and serves as a Director.

Mr. Roussy Newton also founded Latent Capital Ltd. in 2015 and holds the title of Partner. Furthermore, he serves as President & Director. Mr. Roussy Newton is also Chief Executive Officer & Managing Director at BTQ AG, and Chairman & Chief Executive Officer at BTQ Technologies Corp.

Johan Wattenstrom – Co-Founder & Director

Mr. Wattenstrom is a Co-founder and Director of Valour. He is also the Co-Founder and Director of Nortide Capital and was previously the Founder of XBT Provider (now known as Coinshares), which created the world’s first-ever Bitcoin ETP in 2015. He has served on the management committees of several Nordic investment banks. He co-founded Valour in 2019, leveraging his extensive experience in trading, financial products, and brokerage to make digital asset markets more accessible, liquid, and efficient.

Advantage in the Market

Investors sometimes ignore quality small companies because they don’t trade on the NYSE or Nasdaq. Furthermore, they gloss over the strong advantages that can be achieved by flying under the radar.

First-Mover Advantage

DeFi Technologies already has over 60 ETPs across European exchanges. Initially, I worried about the costs of launching too many ETPs, but management outlined that the cost to launch an ETP is around $50,000. The company only needs $675,000 in AUM to maintain profitability in a particular ETP, and it only spends $10,000,000 in operating costs annually—a fraction of its revenue.

The team clearly has streamlined the process of creating an ETP, gaining regulatory approval, and subsequently marketing the new product. By getting to market first with a new coin that is hot, innovative, or an industry staple, DeFi can grab investment dollars faster than the competition. Those assets under management become sticky. And the bigger the ETP grows, the more likely it is to find volume, traders, and new buyers. It becomes a flywheel. Investors and institutions gravitate to the largest and most liquid ETPs.

As I mentioned earlier, DeFi plans to launch another 40 ETPs in Europe next year and expand its business into Singapore, Africa, and the UAE. The company’s AUM could easily double next year, and the list of ETPs is about to grow significantly in 2025.

Investors will choose DeFi’s ETPs because they are fast to market, have significant assets already under management, and offer a broad range of offerings. However, the advantages don’t end there.

The company’s proprietary trading desk, DeFi Alpha, generated nearly $100 million in revenue in 2024 and didn’t have a single losing month of trading. The trading desk’s low-risk arbitrage model suggests that DeFi can continue this streak in 2025. Even if it has a month in the red, we shouldn’t expect the losses to amount to much.

Valour, the asset management business, should generate growth, while DeFi Alpha offers stable and consistent revenue and profits. It is not often we see a small company with a combination of strong financials and multiple market advantages.

Return Potential

Assessing DeFi Technologie’s return potential is relatively straightforward, with one caveat, so let’s get that out of the way first.

The stock trades in Canada and on the OTCQB in the United States. With the Canadian markets as its primary home, the stock is subject to attacks by short sellers. The rules governing short-selling are far less restrictive in Canada, and we’ve heard many stories of attacks on companies, even those with solid fundamentals and strong growth.

Now, let’s jump into DeFi’s return potential.

Three factors drive the stock’s upside: AUM, proprietary trading, and SolFi Technologies.

- Valour ETPs – Assets Under Management

As of December 31, 2024, AUM stood at $819 million, and net monthly inflows were $38.8 million. Management has guided revenue from AUM at 8-10%, so if we assume AUM remains unchanged and there are no net inflows in 2025, revenue for the year will have a midpoint of $73.7 million. That’s our base, and it’s a pretty low one.

Based on existing and anticipated new products and regions, more realistic expectations are for net inflows of around $500 million for the year. The overall sentiment for crypto is bullish in 2025. If we assume a modest 10% growth in AUM, DeFi should end the year with $1.4 billion in assets under management, equating to $126 million in revenue.

These numbers will likely still be below actual results, but using a conservative analysis with smaller companies is better.

- DeFi Alpha – Proprietary Trading

DeFi Alpha has never had a losing month trading for DeFi Technologies. Of course, historical results do not guarantee future returns, but I like the consistency. The second quarter of 2024 was significantly better than the third, but trading tends to be streaky and lumpy.

In 2024, DeFi Alpha generated $96.7 million in revenue without a single losing month. The strategy’s focus on low-risk arbitrage opportunities is the key to this success. Since the methodology is proprietary, we can’t break it down into its parts, but the current track record speaks volumes.

- SolFi Technologies

The market underestimates the benefit the spinout of SolFi Technologies will have on DeFi Technologies’ share price. For months, Microstrategy was the only equity option for investors wanting exposure to Bitcoin through the traditional equity markets. We have watched a dozen companies copy Microstrategy to some degree.

Bitcoin ETFs have made their market debut and accumulated hundreds of millions in assets. Ethereum ETFs have experienced slower growth, but the price action remains muted compared to Bitcoin and Solana.

While the media focuses on Bitcoin, Solana is experiencing incredible growth driven by alt and memecoin trading, finance transactions, and gaming. Daily transactions on Solana dwarves Ethereum. Its low-cost, lightning-speed transactions have attracted integrations from household tech names like Google, Stripe, PayPal, and Shopify.

To construct a valuation for SolFi as a standalone company, we will need details surrounding the underlying operating company, its free cash flow, the amount of Solana (SOL) staked with SolFi from the onset, and the capital structure. Until we have that information, we are left with speculation. Currently, Microstrategy holds about $48B worth of Bitcoin and trades at an $84 billion market, so it is a 1.75x multiple.

It’s important to remember that Microstrategy has all but abandoned its operating business, while SolFi is battle-tested with its DeFi validator and MEV engine. SolFi is already proving that it can create industry-leading yield generation in Solana.

The spinoffs may not end with SolFi Tech. DEFTF may also spin out CoreFi, a leveraged, regulated approach to Bitcoin yield, and CORE, the blockchain’s native asset. CoreFi offers DeFi holders high-beta exposure to Bitcoin and BitcoinFi opportunities, supported by Bitcoin mining hash power, non-custodial staking, and dual staking.

Strong Business Momentum

The next thing to consider is DeFi’s substantial revenue, free cash flow, and valuation compared to similar crypto-related businesses.

By the end of the third quarter, DeFi Technologies already booked revenue of $112 million for 2024. An impressive $71.4 million hit the bottom line, equating to earnings of $0.23 per share. Management forecasted full-year revenue of $141.50 million. Using the same margins as the first nine months of the year, we should anticipate full-year net income of $90.2 million and earnings per share of $0.29.

If shares are trading around $3.20, giving it a market cap of $1 billion, we have a P/E (Price to Earnings) of 11 and a P/S (Price to Sale) of 7.

Coinbase (COIN) trades at a P/E of 48 and P/S of 12. Robinhood (HOOD) trades at a P/E of 84 and P/S of 18. Even Blackrock (BLK) trades at a P/E of 25 and a P/S of 8.

You’ll be hard-pressed to find any asset management companies growing at 40%+ and a P/E and P/S at the level of DeFi Technologies.

The bottom line is between DeFi Technologies’ strong financials, profitability, market advantages, an upcoming spinoff of SolFi Technologies, growing AUM, and potential for an IPO on a senior exchange in 2025, I believe the stock can 5x over the next 12 months and 12x over the next two to three years.

What Could Go Wrong

The DeFi Technologies story almost sounds too good to be true, so what could go wrong?

A deep cryptocurrency bear market and government regulation.

DeFi Technologies survived the last bear market and could survive another one. Unfortunately, a deep bear market could hinder revenue growth and restrict the upside in the company’s valuation.

Valour, the company’s asset management business, is such a large driver of revenue and digital treasury growth that a drop in cryptocurrency prices would likely lead to a drop in revenue.

While the company has produced positive net inflows to its ETPs every month for two years, the trend hasn’t shown that the inflows could outpace value depreciation in a bear market. In other words, the loss of value of the underlying AUM would exceed the gain in AUM from net inflows.

Given the current administration supports advancements in the use of cryptocurrency, another bear market is unlikely, so I view the risk potential as low; however, it is not zero.

The new administration’s support for cryptocurrency is both a positive and a potential negative for DeFi Technologies. This is one of those rare cases where the risk of government regulation is likely what you think it is.

Because the new administration has demonstrated a favorable attitude toward cryptocurrency, it may influence regulators to grant new US-based cryptocurrencies on many more coins than Bitcoin and Ethereum. If that is the case, we could see Blackrock or another major ETF player expand rapidly and offer a family of ETFs similar to DeFi Technologies’ ETPs.

Furthermore, a bigger player could offer better terms, such as lower management fees or a share of staking rewards, to entice investors to their products. That may result in net outflows from DeFi’s ETPs or the company having to cut fees to maintain AUM. I view this as a moderate risk, although the more likely outcome is that one of the more significant financial institutions simply buys DEFTF rather than starting from scratch.

How to Invest

DeFi Technologies’ story has two parts: its fast-growing financial products business, which focuses on cryptocurrency exchange-traded products (ETPs), market making, and prop trading, and its forthcoming SolFi spinoff.

Investing directly into SolFi isn’t an option for us today. While we could wait for DeFi to spin SolFi into a standalone public company, we may be left chasing the stock price, especially once the broad market understands what SolFi offers investors. We anticipate headline comparisons to Microstrategy will come quickly, and demand will follow.

However, by owning shares of DeFi Technologies, you and I gain exposure to SolFi before nearly everyone on Wall Street.

Putting Money to Work

DeFi Technologies’ growth has exploded over the past year and shows no signs of showing. As assets under management build, DeFi’s upside potential exponentially increases while the risk at the current valuation reduces. The approaching spinoff of its SolFi business provides a second catalyst for DeFi’s valuation. Plus, we believe it will be an attractive standalone holding as the market will view it as the “MicroStrategy of Solana.”

While I’m thrilled with DeFi Technologies’s accomplishments over the past two years and plan to buy additional shares in my personal account, I still want the company to aggressively pursue its planned U.S. IPO on a senior exchange over the next 12 months. Remember, the company already filed its 40-F in September 2024.

An IPO on a senior U.S. exchange will dramatically increase the number of institutions that can buy the stock and analysts that will cover it.

DeFI Technologies is listed on the OTCQB under the symbol DEFTF.

Although the stock is very liquid, I recommend using limit orders to purchase shares as a rule of thumb. The shares closed on Wednesday at $3.15, and through limit orders, you can begin buying shares up to $3.75.

I plan to buy a small block near current levels and bid for additional shares on dips and pullbacks over time. This isn’t a short-term trade, so we can be patient with accumulating a position over time.

Disclosure: Tim Collins is a shareholder and active consultant for DeFI Technologies through their ownership in an unrelated investment venture.

IMPORTANT NOTICE AND DISCLAIMER

Neither the author nor the publisher, Streetlight Confidential, was paid to publish this communication concerning DeFi Technologies. The publisher’s owners were previously paid through an unrelated business venture by DeFi Technologies for consulting and business development services. However, neither the consulting services nor the compensation were related to the publisher’s recommendation herein. The publisher’s owners own shares in DeFi Technologies purchased in their personal accounts. The publisher’s owners, therefore, have an incentive to see DeFi Technologies perform well. This share ownership should be viewed as a major conflict with our ability to be unbiased. The publisher’s owners have no present intention to sell any of the issuer’s securities in the near future but also do not undertake any obligation to notify the market if and when they decide to buy more or sell shares of the issuer. For these reasons, we stress that you conduct extensive due diligence as well as seek the advice of your financial advisor or a registered broker-dealer before investing in any securities.

Readers should beware that third parties, profiled companies, and/or their affiliates may liquidate shares of the profiled companies at any time, including at or near the time you receive this communication, which has the potential to harm share prices. Frequently, companies profiled in such articles experience an increase in volume and share price during the course of investor awareness marketing, which may end as soon as the investor awareness marketing ceases. The investor awareness marketing may be as brief as one day, after which a decrease in volume and share price may occur.

This communication is not, and should not be construed to be, an offer to sell or a solicitation of an offer to buy any security. Neither this communication nor the publisher purport to provide a complete analysis of any company or its financial position. The publisher is not, and does not purport to be, a broker-dealer or registered investment adviser. This communication is not, and should not be construed to be, personalized investment advice directed to or appropriate for any particular investor. Any investment should be made only after consulting a professional investment advisor and only after reviewing the financial statements and other pertinent corporate information about the company. Further, readers are advised to read and carefully consider any risk factors identified and discussed in the advertised company’s investment materials and/or government filings. Investing in securities, particularly securities of private companies, is speculative and carries a high degree of risk and illiquidity. Past performance does not guarantee future results. This communication is based on information generally available to the public and does not contain any material, non-public information. The information on which it is based is believed to be reliable. Nevertheless, the publisher cannot guarantee the accuracy or completeness of the information.

FORWARD-LOOKING STATEMENTS. This publication contains forward-looking statements, including statements regarding the expected continual growth of the featured companies and/or industry. The publisher notes that statements contained herein that look forward in time, which include everything other than historical information, involve risks and uncertainties that may affect the companies’ actual results of operations. Factors that could cause actual results to differ include but are not limited to, changing governmental laws and policies impacting the company’s business, the size and growth of the market for the companies’ products and services, the companies’ ability to fund its capital requirements in the near term and long term, pricing pressures, etc.

INDEMNIFICATION/RELEASE OF LIABILITY. By reading this communication, you acknowledge that you have read and understand this disclaimer, and further that to the greatest extent permitted under law, you release the Publisher, its affiliates, assigns and successors from any and all liability, damages, and injury from this communication. You further warrant that you are solely responsible for any financial outcome that may come from your investment decisions.

TERMS OF USE. By reading this communication you agree that you have reviewed and fully agree to the Terms of Use. If you do not agree to the Terms of Use, please contact the publisher to discontinue receiving future communications.

INTELLECTUAL PROPERTY. Streetlight Confidential is the publisher’s trademark. All other trademarks used in this communication are the property of their respective trademark holders. The publisher is not affiliated, connected, or associated with, and is not sponsored, approved, or originated by, the trademark holders unless otherwise stated. No claim is made by the publisher to any rights in any third-party trademarks.